Announcement: Lorem ipsum dolor sit amet, consectetur adipiscing elit. Donec et quam blandit odio sodales pharetra.

Announcement: Lorem ipsum dolor sit amet, consectetur adipiscing elit. Donec et quam blandit odio sodales pharetra.

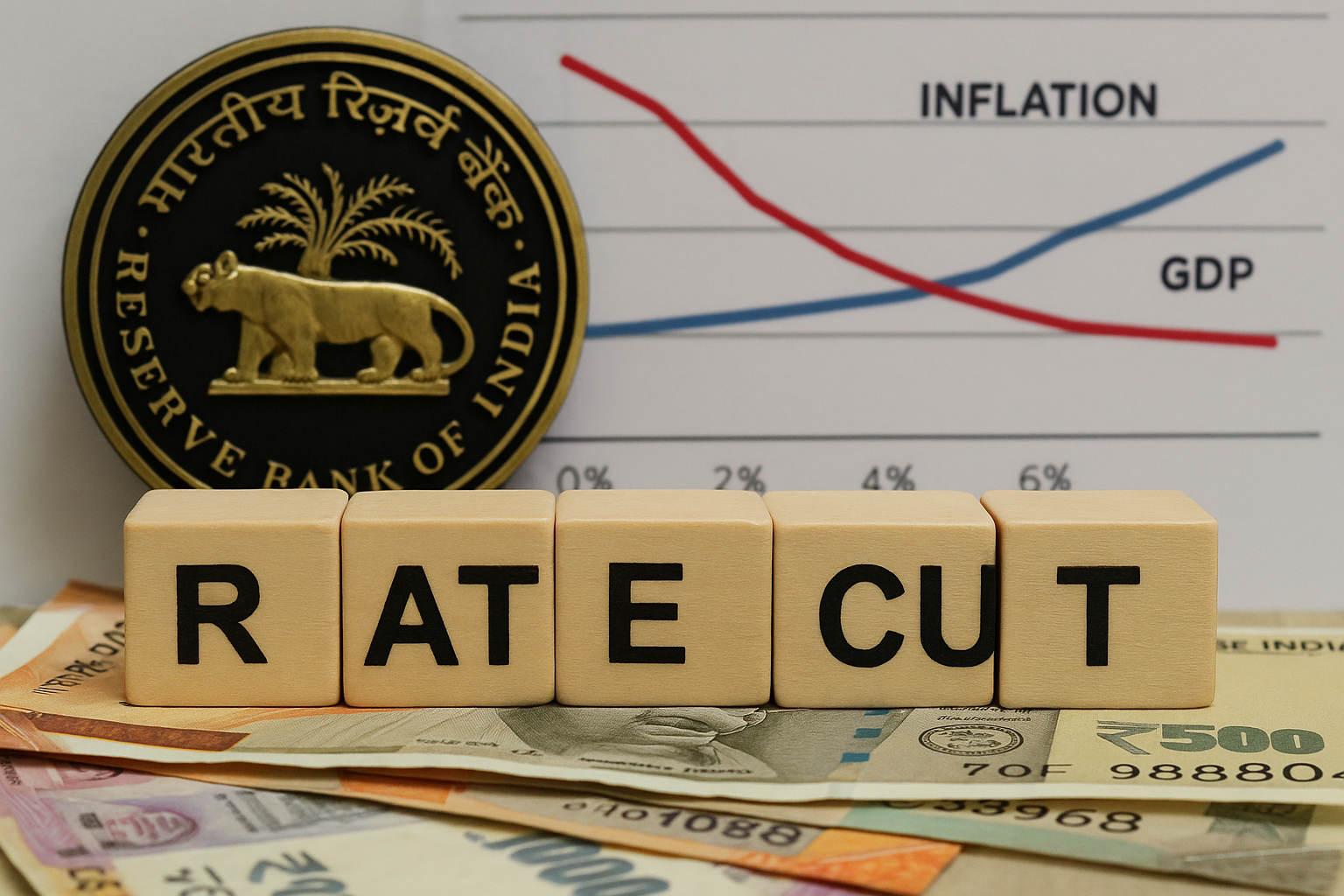

Why is RBI still hesitant to cut repo rates, despite low inflation?

During the week, the RBI published the minutes of the October MPC meet. While all members agree on inflation remaining low, they are still hesitant to recommend a rate cut. Why this apparent dichotomy?

Written by: SERNET Research Team

Table of Content

Gist of the inflation story

Normally, the sharp fall in the consumer inflation should have driven more than aggressive rate cuts by the RBI. Inflation has fallen to 1.54%; much lower, even than the lower end of the range of 2%. In the past, a fall in inflation would have triggered more rate cuts, but the RBI feels this is time for caution. While RBI has already cut rates by 100 bps since February 2025, the repo rates at 5.50% are still above the pre-COVID rates. So, what exactly is stopping the RBI MPC from more rate cuts? Apparently, there are 3 reasons driving this hesitancy.

Does India need rate cuts?

That is the million-dollar question. In the first quarter of FY26, GDP growth was much better than expected at 7.8%. It appears like the GDP growth really does not require any boost from the center. The natural momentum of economic activity appears to be good enough. The other argument is that; since the level of inflation is so low, real GDP growth has an automatic advantage. That is, again, an irrefutable logic. More importantly, it is the general view in the RBI MPC, that any future growth support must come from the fiscal side; not monetary side!

Holding back its ammunition

As one browses through the minutes of the RBI MPC, one thing is clear. There is a growing concern over the impact of global events. We have already seen the impact that the tariffs are having on the trade deficit, which widened to $32.15 billion in September. MPC members do expect that the combination of tariffs, the US shutdown, and the H1-B visa rules; will start to impact India’s growth some time in the near future. At that point, the RBI needs a lot more monetary firepower at its disposal. The feeling, and rightly so, is that rate cuts at this juncture may not have the desired impact on growth. The RBI can instead keep these tools in the reserve, should GDP growth deteriorate.

Rupee could be another factor

One reason the RBI MPC was loath to a rate cut could be the rupee. The USDINR has already weakened to near ₹89/$. In the previous week, RBI governor also spoke about speculative attacks on the Indian rupee in the offshore markets. While the RBI does have large reserves to defend the rupee, it must avoid any economic measure that has the potential to weaken the Indian rupee. That is what can happen if rates are cut at this point. The rupee is already under pressure, and any move by the RBI to cut rates could impact portfolio flows and also result in a sharp weakening of the rupee. That is something, that the RBI and Ministry of Finance want to avoid at this point!

Comments